HO-3 vs HO-5 Home Insurance Policy: Which One Should You Choose?

Published on July 7, 2025

Sarah Patel

Homeowners & Property Insurance Expert.

Sarah Patel is a property underwriter-turned-writer with 10 years in the field; she focuses on flood, wildfire, and replacement-cost planning for homeowners.

Introduction

When shopping for homeowners insurance, two policy types dominate the market: HO-3 and HO-5. While both provide protection for your home, they differ in how they cover personal property and how comprehensive their protection is.

Understanding the distinctions between HO-3 and HO-5 policies is critical for choosing the right homeowners insurance that balances cost with coverage — especially if you’re insuring a high-value home or expensive belongings.

What Is an HO-3 Policy?

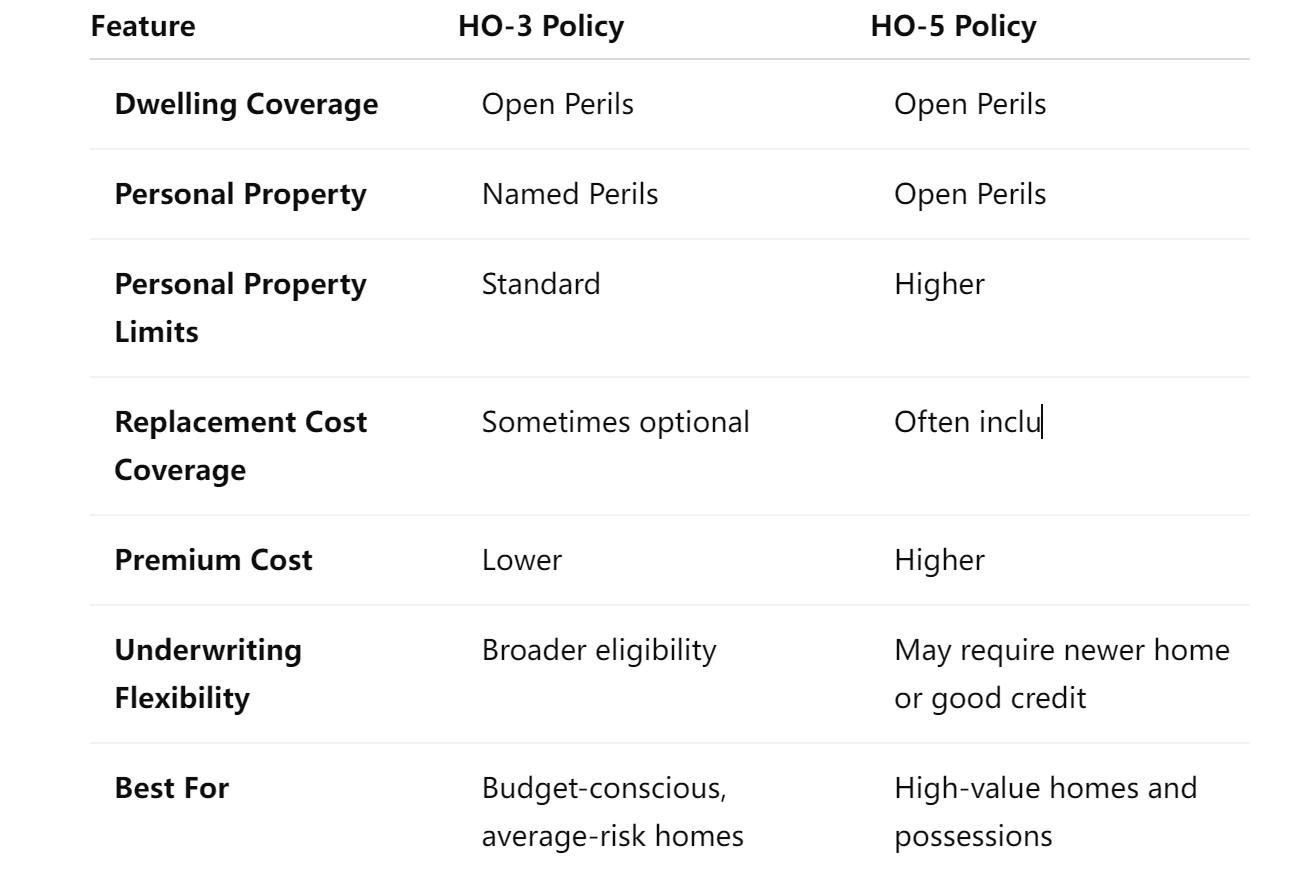

The HO-3 policy, also called the “Special Form,” is the most popular type of homeowners insurance in the U.S. It offers strong coverage for your house (the structure), but more limited protection for your belongings.

✅ HO-3 Key Features:

- Dwelling coverage: Protected on an open-perils basis — covers all causes of loss unless specifically excluded.

- Personal property coverage: Protected on a named-perils basis — only specific events (like fire or theft) are covered.

- Affordable premiums: HO-3 policies typically cost less than HO-5.

🔍 What Does HO-3 Cover?

Your structure is protected broadly, but personal items like electronics, jewelry, and clothing are only covered if damage or loss results from these named perils:

- Fire and smoke

- Windstorm or hail

- Lightning strikes

- Theft or vandalism

- Falling objects

- Water damage from plumbing failures

This means an HO-3 policy may exclude more personal property risks, especially for high-value items or unusual damage scenarios.

What Is an HO-5 Policy?

The HO-5 policy, often called the “Comprehensive Form,” provides broader, more robust homeowners coverage. It’s usually recommended for newer homes or homeowners with high-value personal property.

✅ HO-5 Key Features:

- Dwelling & personal property: Both are covered on an open-perils basis.

- Fewer exclusions overall.

- Higher coverage limits for personal belongings.

- More generous replacement cost terms.

🔐 Who Is HO-5 Best For?

- Homeowners with valuable possessions (e.g. luxury electronics, designer furniture)

- People who want fewer surprises during the claims process

- Those living in low-risk areas where premiums remain manageable

HO-3 vs HO-5: Side-by-Side Comparison

Choosing the Right Policy for Your Needs

Choose HO-3 if:

- You want essential homeowners insurance at a lower cost.

- You don’t own a lot of expensive items.

- You’re comfortable with named-peril coverage for personal property.

Choose HO-5 if:

- You want comprehensive homeowners insurance with fewer exclusions.

- You own expensive items (camera gear, artwork, designer clothes).

- You prefer peace of mind over upfront savings.

Example:

A burst pipe damages your home office and electronics:

- HO-3 may only partially cover the damaged electronics, depending on if water damage is a named peril.

- HO-5 likely covers it, unless water damage is explicitly excluded.

Frequently Asked Questions (FAQs)

❓ Is HO-5 better than HO-3 for every homeowner?

Not always. HO-5 offers broader protection, but at a higher price. If you live in a lower-risk area and don’t need open-peril personal property coverage, HO-3 may be more economical.

❓ Can I switch from an HO-3 to an HO-5 policy?

Yes. Most insurers allow you to upgrade at renewal, as long as your home qualifies. Factors include the home’s age, construction materials, and your credit score.

❓ Are HO-5 policies harder to qualify for?

Typically, yes. HO-5 policies may require your home to be newer, well-maintained, or located in a low-claim-risk area.

❓ Does HO-5 cover everything?

No insurance policy covers everything. Even HO-5 excludes events like floods, earthquakes, and normal wear and tear. You may need add-on policies or riders.

Conclusion: Which Homeowners Insurance Policy Is Right for You?

Both HO-3 and HO-5 policies provide valuable protection, but choosing the right one depends on how much coverage you want, what you own, and what you can afford.

- If you're seeking affordable homeowners insurance with solid structural coverage, HO-3 may meet your needs.

- If you're looking for the best homeowners insurance for high-value items, or want fewer coverage gaps, HO-5 is likely the better option.

Whichever policy you choose, make sure you compare quotes and understand the exclusions.

You Might Also Like

9 Critical Steps for Getting Home Insurance After a Claim in 2025

Aug 1, 2025Top 17 Must-Know Facts About Home Insurance for Condos 2025

Aug 1, 2025Home Insurance for First-Time Buyers: 2025 Checklist

Jul 10, 20255 Proven Strategies to Lower Your Homeowners Insurance Premium in 2025

Jul 8, 2025What Is Home Insurance and How Does It Work in the U.S.?

Jul 2, 2025